Bank of Japan Explores Tokenized CBDC: A Digital Yen Could Reshape Asia’s Crypto Landscape

When one of the world’s most conservative central banks starts seriously discussing tokenization, markets pay attention. The Bank of Japan is now evaluating the potential issuance of a tokenized central bank digital currency (CBDC) — a move that could significantly influence not only Japan’s financial infrastructure but the broader trajectory of digital assets in Asia.

Japan has historically approached crypto regulation with caution but clarity. Now, the conversation is shifting from oversight of private digital assets to the state’s direct participation in tokenized money. That transition marks a structural evolution — not just a policy update.

As someone who has spent more than a decade analyzing fintech and blockchain infrastructure, I view this development as part of a broader global recalibration: central banks are no longer asking whether tokenization matters, but how they should implement it.

Why a Tokenized CBDC Matters Now

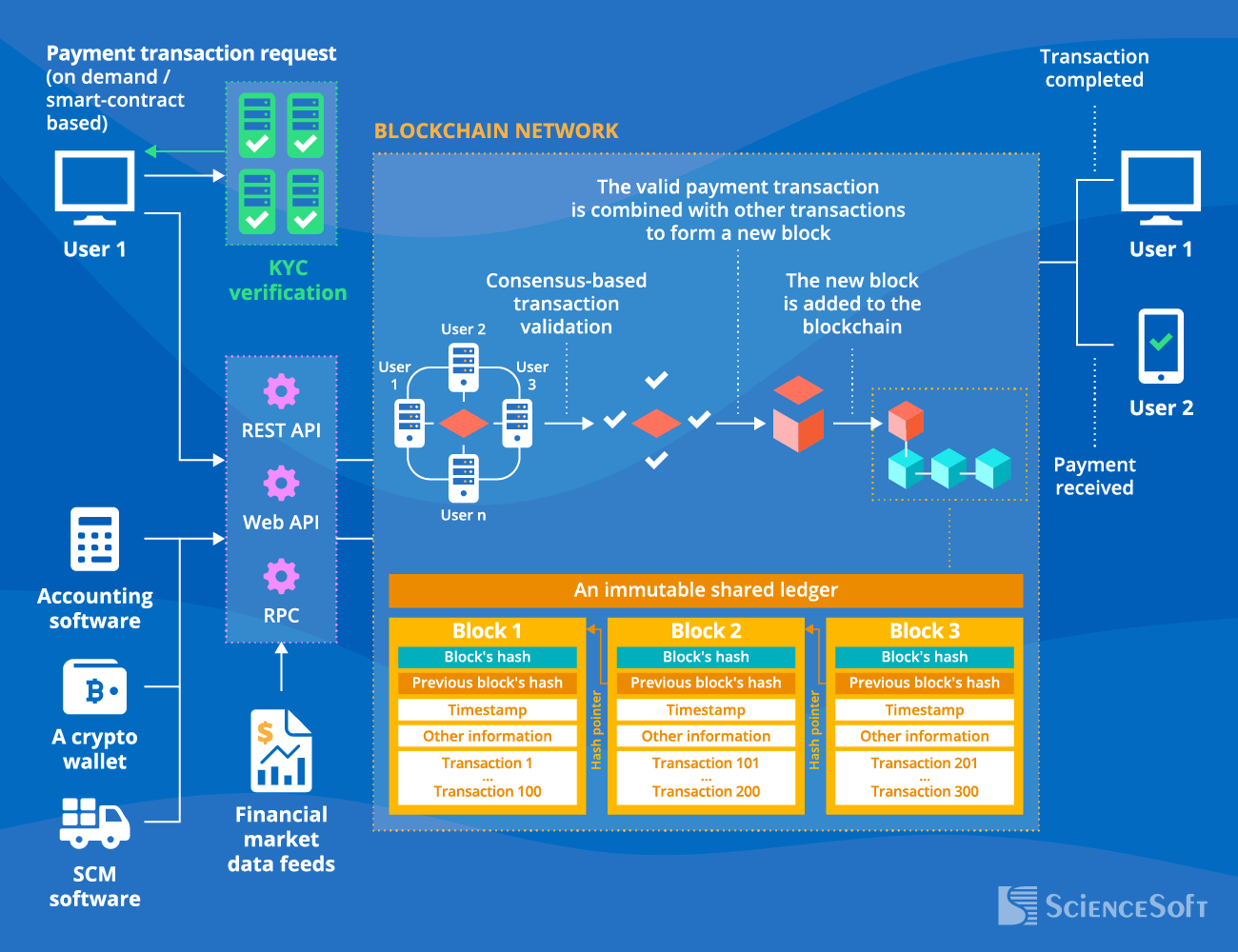

A tokenized CBDC differs from a simple digital representation of fiat currency. While many countries already operate digital banking systems, tokenization implies blockchain-inspired architecture — potentially programmable, traceable, and interoperable.

For Japan, several strategic motivations stand out:

- Modernizing domestic payment infrastructure

- Increasing settlement efficiency

- Competing with regional digital currency initiatives

- Reducing dependence on private stablecoins

- Preparing for cross-border programmable finance

Asia has become a proving ground for CBDC experimentation. China’s digital yuan has already seen large-scale pilot deployments. If Japan advances toward a digital yen, it signals regional escalation in sovereign digital currency adoption.

CBDC vs Stablecoins: Strategic Competition or Coexistence?

One of the most important questions for crypto markets is how a Japanese CBDC would interact with private stablecoins such as USDT or USDC.

A tokenized digital yen could:

- Offer state-backed stability

- Reduce reliance on dollar-denominated stablecoins

- Introduce programmable compliance features

- Increase regulatory visibility over capital flows

However, CBDCs and stablecoins serve different ecosystems. Stablecoins thrive in permissionless DeFi environments. A central bank-issued digital currency will likely operate within stricter frameworks.

This creates a dual-track system: regulated sovereign digital money alongside decentralized liquidity layers.

Regulatory Implications for Crypto Markets

Japan has long been one of the more structured regulatory environments for crypto exchanges. A digital yen initiative would likely deepen integration between regulated crypto platforms and traditional financial infrastructure.

Potential ripple effects include:

- Clearer compliance standards for exchanges

- Enhanced AML and transaction monitoring

- Tokenized asset settlement improvements

- Cross-border interoperability experiments

From a macro perspective, CBDCs strengthen the regulatory perimeter around digital finance. That can be interpreted in two ways: tighter oversight, or greater legitimacy.

Both can coexist.

Infrastructure, Not Ideology

It is important to avoid ideological framing. This is not a “crypto vs government” development. It is an infrastructure evolution.

Tokenization improves:

- Settlement speed

- Transparency

- Auditability

- Programmability

The real question is architectural design. Will the Bank of Japan adopt a permissioned ledger model? Will it allow API integrations with private fintech firms? Will interoperability with public blockchains be explored?

Those details will determine whether the digital yen becomes a closed financial instrument or a bridge between traditional finance and blockchain ecosystems.

Geopolitical Context: Asia’s Digital Currency Race

Regional dynamics cannot be ignored. Asia’s financial centers are competing to define next-generation payment standards. A tokenized yen would position Japan as a serious participant in the future of programmable finance.

Cross-border settlement corridors — particularly between Japan, Singapore, and potentially China — could redefine trade settlement efficiency in the region.

Moreover, global investors will watch closely. CBDC progress from a G7 economy increases legitimacy for blockchain-based financial rails.

Market Reaction: Limited Short-Term Volatility, Long-Term Significance

In the immediate term, crypto markets may not react dramatically to exploratory CBDC discussions. Traders typically respond to liquidity and macro catalysts, not policy research phases.

But structurally, this matters.

CBDCs reinforce a critical thesis: blockchain architecture is not fringe technology — it is becoming institutional infrastructure.

As I often note in my regulatory analysis:

“The future of digital finance won’t be defined by whether governments adopt blockchain principles — it will be defined by how they integrate them without undermining open innovation.”

Japan’s measured approach suggests deliberation rather than haste. That is consistent with its financial policy tradition.

What Comes Next?

The next phase will likely involve:

- Pilot testing frameworks

- Technical architecture disclosures

- Industry consultation with fintech firms

- Legislative coordination

For crypto markets, the implications are nuanced. Increased state participation in tokenized money may tighten compliance — but it also validates the foundational technology that decentralized finance was built upon.

If the digital yen progresses beyond research into structured pilots, Asia’s crypto landscape could enter a new phase of institutional integration.

And when infrastructure evolves, markets eventually follow.